Macro Note (April 2023)

Yes, it is now May, the April note is quite late due to laziness and the allure of Portuguese beaches. Data/Commentary current from mid-April. US Econ Data in focus, RoW and Markets in May 2023 Note

Summary:

Econ data still weakening, but certainly holding up better than expected in some places likely due to “excess savings” and bigger than budgeted fiscal in the US.

China reopening still an unknown quantity (how sheepish are Chinese consumers after being whacked by zero covid and a real estate crisis), however there seems to be a renewed fiscal impulse into (unproductive) investment (unsure if really “stimulus” yet), which could improve demand conditions globally in the short term. Large risk to base case of imminent global recession, TBC.

The baby-banking crisis during the month was the first serious cracks showing in the edifice. Unlikely to be the last. Further discussion below on causes/effects and implications.

Rates markets are a complete mess, apparently caught between the economy ostensibly holding up (“higher for longer”) and banks collapsing. The distribution of outcomes for the end of the year is rates at ~5% or back to near 0% (ignore the “3 cuts priced in for 2023” nonsense from the pundits), not healthy or easy to manage basis risk. Can’t forget that caution can be self-fulfilling (individually rational and systemically toxic e.g. a bank run).

OPEC+ is not fucking around. They were clearly not happy with Brent having a 70 handle. Cheap energy not coming back anytime soon outside of a really ugly demand picture. Additionally, potentially some signal here for future demand weakness?

Overall, 2023 recession more likely given the banking issues. Econ data already weakening, and credit conditions likely to tighten rapidly in the aftermath of this event.

Oft underdiscussed as a large underlying force on econ activity is collateral values. As part of the credit cycle: Increasing optimism > New credit > Upward pressure on asset prices (+ more increasing optimism) > More collateral for borrowing > New credit. Repeat. This is the ‘virtuous’ part of the credit cycle. Massively oversimplifying, rising rates has put this cycle into reverse and will likely play out over a number of years unless interrupted.

Econ Data

US Economy

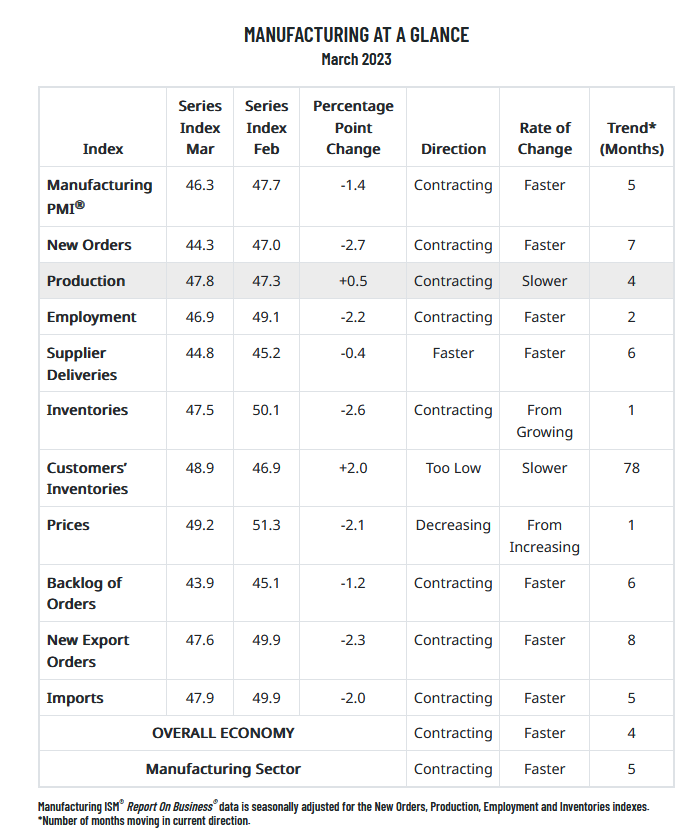

The ISM PMI (survey data, diffusion indexes) for US manufacturing has been in contractionary territory for 5 months and is accelerating. The services PMI is holding up ok, but worth nothing that the cyclical elements of the economy lead into recessions and weakness likely won’t show in services until it’s too late.

Focus is on “New Orders” (and new export orders) as they are the most leading elements.

Industrial production came in ok in March. With some upward revisions, the survey weakness not showing sharp deterioration but certainly not much growth.

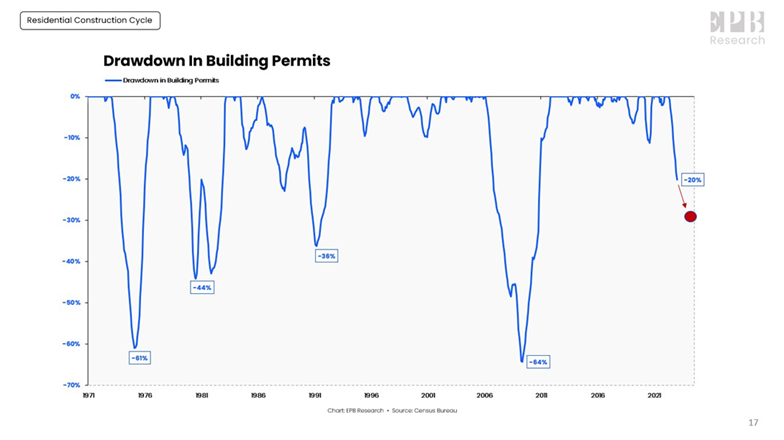

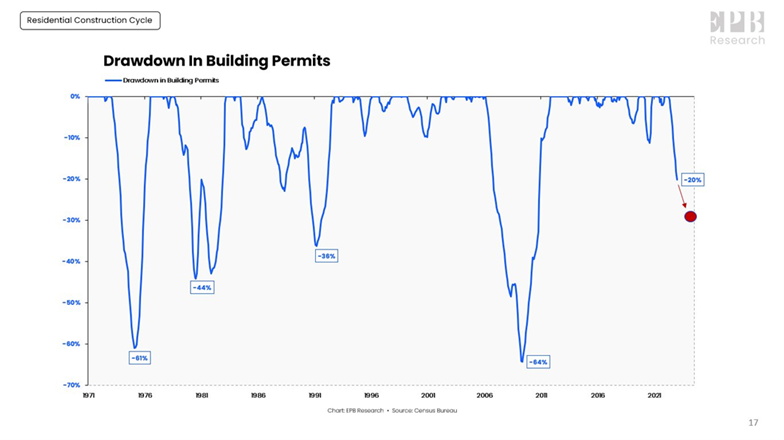

US housing activity appears to be rolling over. Drawdown in building permits is a good leading indicator of future activity. Flashing orange.

Chart from @EPBReseach on twitter, a lot of great macro content on his twitter feed and youtube channel which is great for all levels of accumen.

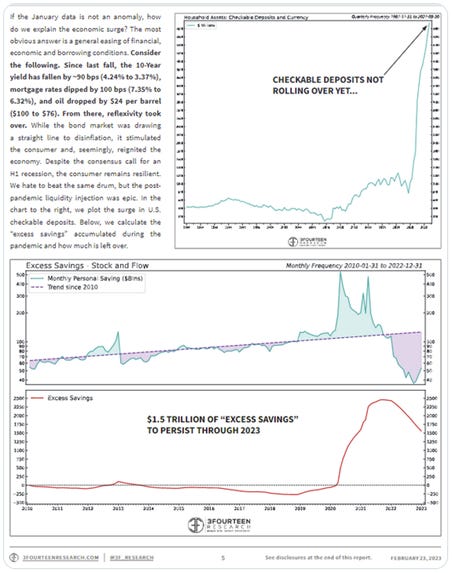

Excess consumer savings is still the biggest driver of uncertainty for strength in the US economy, how willing are they to draw this down before they tighten their belts?

Remember “Excess savings” is really implying that consumers will readily draw down what they were given “above trend” all the way back to trend before cutting consumption. While this certainly may be true for some who will need to spend their accrued excess to cover expenses, others will want to hold on to their windfall. Therefore, the distribution of these gains is important, and much is held in the upper quintiles of the US population.

Good chart from Warren Pies, a couple of months old now tho. Note the level of excess savings is dependent on where one draws the initial trend line so estimates vary wildly. I think the important part is that they are being drawn rapidly, and what happens to corporate earnings and economic activity when this force is exhausted. Hangover.

A lot of Jan data that surprised to the upside across the board – Jobs, hours, Retail Sales, PMI’s etc have rolled back over, suggesting that was in fact seasonal adjustment noise.

My underlying assumption is that seasonal adjustments have been broken by covid and this has exacerbated the already present problem of “Fog of Cycles” as @Kayfabecapital eloquently coined.

Jobless claims support the idea of general resilience. However, Quits & Openings seem to have rolled over. Jobs always lag, don’t rely on them to get a read on the economy.

Initial claims and continued claims are slowly ticking up, and given employment is a lagging indicator, this is a confirmatory sign of weakness rather than a counterpoint.

Fiscal Impulse

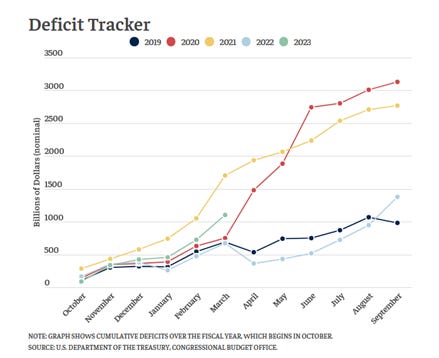

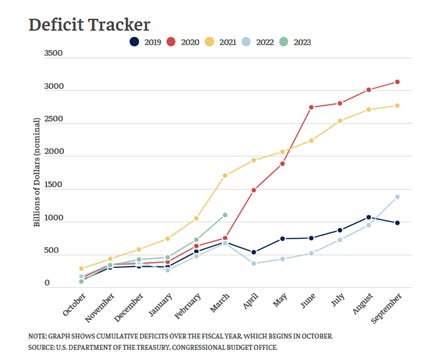

As noted last month, for FY23 the US Federal Budget Deficit is budgeted to be $1.4tn. However, as at March the deficit is already $1.1trn and with a lower expected tax season (much less cap gains), it is unlikely the full year will end the year anywhere near below $1.4trn. This is an economic tailwind and could forestall a recession (but prolong “inflation”)

As a side note on tax season, with tax payments coming up, that is a big liquidity drain from markets generally, interesting to see how that plays out this year in a fragile system. Sell in May and go away?

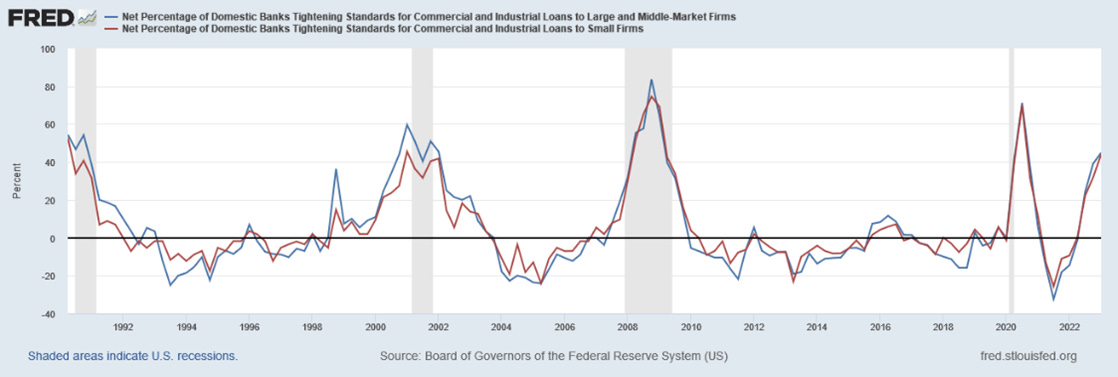

Credit Impulse

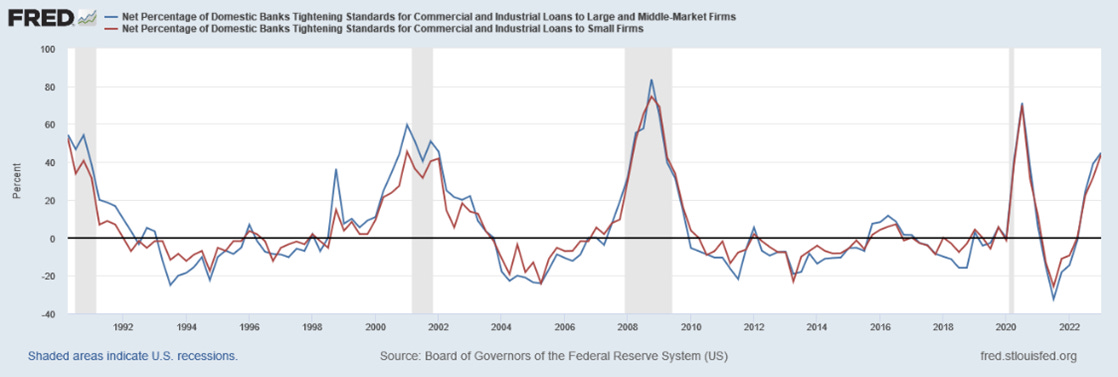

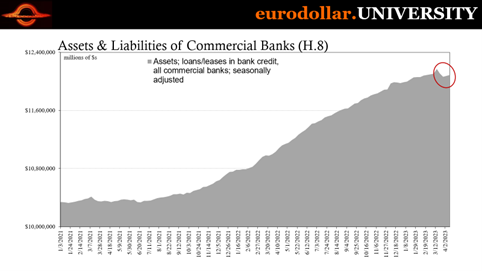

Post the baby-banking crisis we will likely see sharp reductions in bank lending. Strangling an economy of credit is a quick path to a recession, to avoid recession we need to see this line moving up, sideways is not enough.

Tightening lending standard is a bad omen for credit creation.

In last months report, it was clear that the US economy had turned down, it is now clear that we are on a path to recession unless something intervenes.

May Note will include RoW and Markets analysis (along with updated US info).

Special Note: Duration Risk v Credit Risk

Much of our attention is rightfully directed at “Credit Risk”, which is a measure of the additional cost of borrowing (above the “Risk-free” rate) to account for default risk (can the counterparty actually repay?)1

This was of course a huge issue in the GFC, where credit spreads blew out so far (representing a sharp deterioration in liquidity) that rolling financing arrangements was largely impossible, and chaos ensued as levered players blew up in the mad scramble for (good) collateral.

The situation is quite different today. Spreads have thus far behaved well. However, the “risk-free” part of total rate (that is Risk-free + credit spread = total rate) has not. Sometimes people forget that “risk-free” refers to credit risk, there is still duration risk.

Put simply, “Duration” is the sensitivity to the price of a security to a change in interest rates. Duration increases the longer the term of the cash flows. (The details aren’t important, so don’t fret).

So as rates have declined for the past 40 years, long duration has paid off handsomely (the value of long duration assets increases as rates fall), encouraging more and more to take on duration risk. It’s been all one way for a long time.

More recently, as rates have risen, long duration assets have suffered the reverse of this effect.2

This is obviously painful for holders of long duration assets. A system which gorged itself on duration and is levered against the value of that collateral, which is now falling, faces significant risks. Risks that, in aggregate cannot be hedged (these hedges are zero sum). So the pain must be felt somewhere.

Thanks for reading. Hopefully, you found this helpful or interesting.

Feel free to provide questions/comments/feedback.

Subscribe to get new notes as they are released.

Homework (/Sources)

Good thread on construction cycles:

https://twitter.com/EPBResearch/status/1633103320079269890

EPB “How to predict a recession”:

“Excess Savings” Discussion:

https://twitter.com/WarrenPies/status/1644424945210982401

“Fog of Cycles”:

https://twitter.com/kayfabecapital/status/1647698050192736258

It also reflects more market risks like liquidity.

Note that assets are not just priced on spot rates, but the future expectations of rates, so that’s why genuine “higher for longer” would crush duration in a way fund feds being 5% will not.