Macro Outlook (March 2023)

Summary

Econ data in a downward trend.

Avoiding a recession largely relies on a strong China reopening and or renewed US fiscal impulse (both possible).

Rates would fall in a recession scenario, but this is unlikely to protect financial assets (risk aversion overpowers loose money) in the short term.

If a recession is avoided, this will almost certainly mean rates will be in the “higher for longer” scenario.

In the context of financial assets, it seems - Bad news is bad news, and good news is bad news.

This is the exact opposite of the last 15 years where good news was good because it was non-inflationary (therefore no risk of a rates shock like now) and bad news was good news as this would mean looser monetary conditions.

The perceived change in inflation regimes being the key difference in interpretation. Remember, Central Bankers’ primary mandate is “stable prices”, inflation is the biggest risk to their jobs (and the economy).

Overall, it seems like we are on a knife edge. I lean toward recession (already or soon to begin), but can see a wide path to another 6-12 months of ok growth and continued inflationary pressure (then probably worse recession). Either way looks bad for financial assets.

Economic Conditions

Econ Data

Jan data surprised to the upside across the board – Jobs, hours, Retail Sales, PMI’s etc. While the breadth is convincing, there is room to consider fading this news which has pushed many into the “Higher for longer” camp:

Huge seasonal adjustments in Jan;

All contrary to recent trends (i.e. is it just one month in noisy data?);

Econometric models notoriously bad at turns (probably worth whole technical note on this).

The US economy has clearly turned downward, what is unclear is whether this is a gully or a canyon.

Jobless claims support the idea of general resilience. However, Quits & Openings seem to have rolled over (decide for yourself if that tick up in openings is just noise).

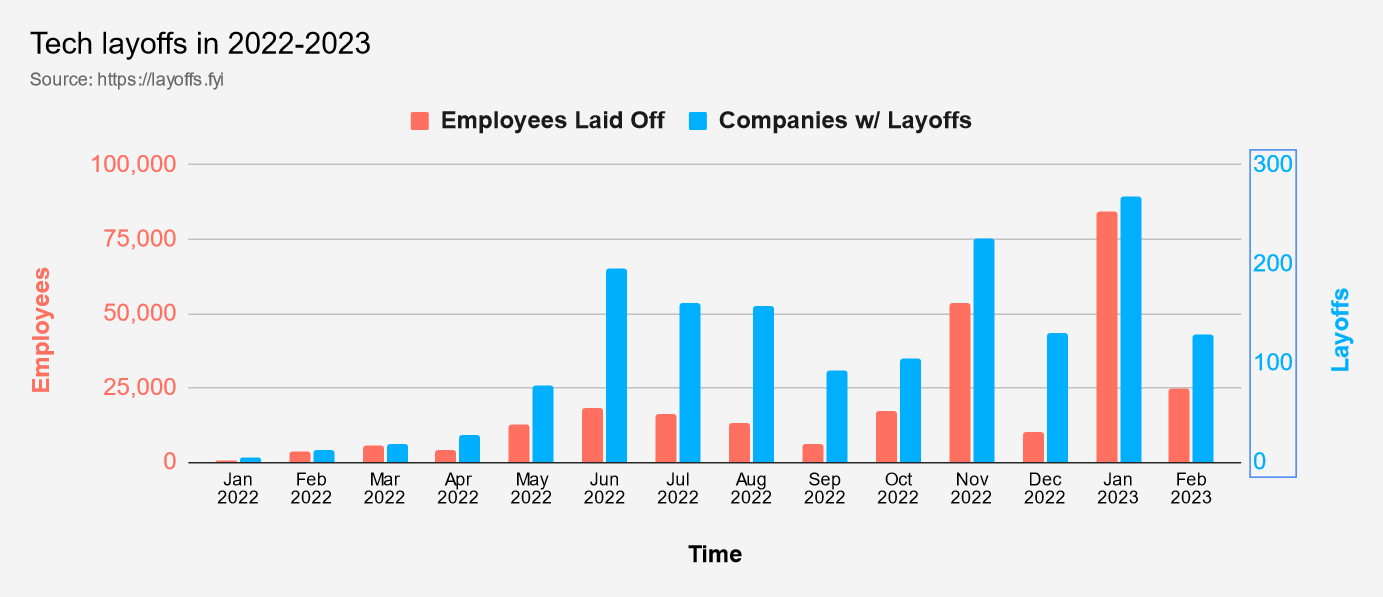

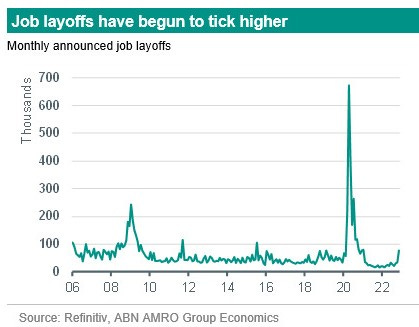

A lot of high profile layoffs announced recently, many of which haven’t been effected yet.

Additionally, these are clustered in more “white-collar” sectors. Interesting in that usually “blue-collar” cyclical part of the economy (housing & manufacturing) generally lead job losses (but also, job loss data tend to be late to the recession party).

The white-collar worker might be less inclined to file an unemployment claim immediately, which may explain the claims data, however, they may also just be finding another job easily.

Worth noting that the higher income earners have a much larger footprint on consumption (and capital markets flows), so theoretically much fewer job losses required to impact aggregate demand/financial flows.

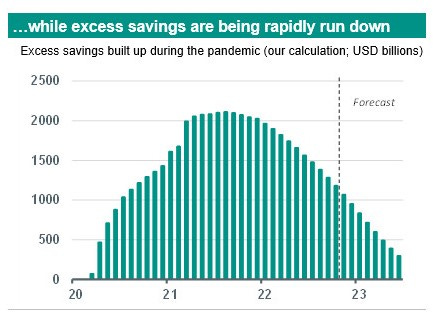

The consumer held up throughout 2022 better than expected, this was likely due to the large stock of “excess savings” accumulated during the pandemic & the ongoing suspension student loan payments etc.

$2.1tn at peak, roughly $1tn at Dec 22, but not evenly distributed, likely that the majority of these savings are sitting with the wealthy, but potentially this could keep us out of recession and inflation pressures on if consumers keep spending.

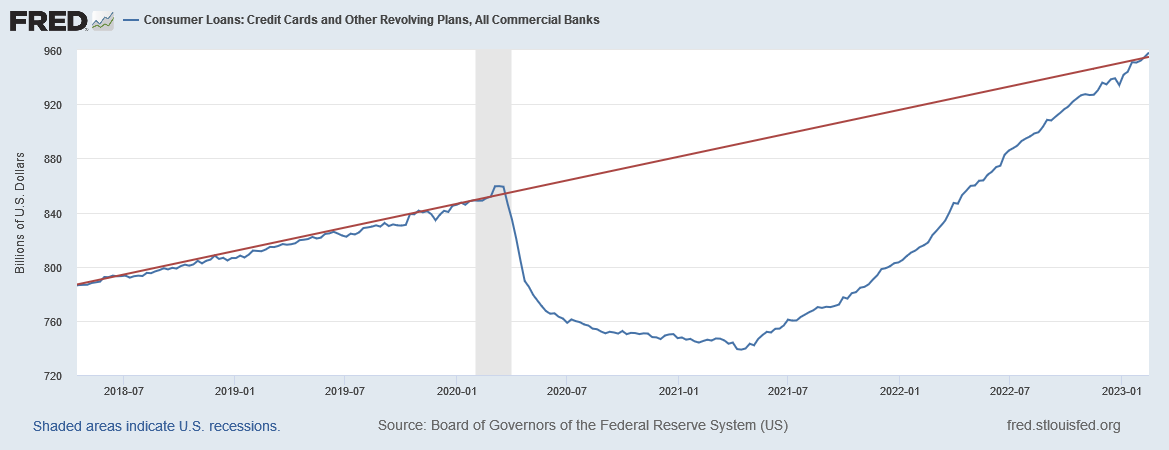

Credit card debt rising rapidly is a tell that perhaps lower income households have already depleted their stock of savings and are feeling the pinch of falling real wages. However, we are not just back on the pre-covid trend, so there are a few interpretations.

Excess savings is a loose concept and there is not guarantee consumers keep running them down as they have over the last 12 months. The decision of what to do with this $1tn will be the deciding factor of when a recession may begin (that and China reopening).

Overall, it is a choose your own adventure scenario presently – Recession or Higher for Longer, Feb and March econ data likely won’t help tell us what is the economic reality but will be extremely important for the short end of the rates curve (Fed reaction function).

Fiscal Impulse

The Fiscal Impulse is useful for understanding cash flowing into the real economy (which shows up as corporate earnings, domestic private savings, and foreign savings (accounting identity) in the immediate term).

For FY23 the US Federal Budget Deficit is $1.4tn, compared to $1.3tn in FY22. Despite the rise, the figure is almost equal in % of Nominal GDP terms (5.2% v 5.3%)

Net interest expense is up $165bn yoy and should mostly flow to holder of financial assets and stay in the financial economy (i.e. not helpful for main street in the way infrastructure spending is). So overall, with drawdowns in excess savings slowing (which is just delayed fiscal), the fiscal impulse appears to be slowing. However, this is just Federal, spending at other levels of government needs to be considered.

Credit Impulse

Large increase in Commercial & Industrial loans in 2022. Three broad interpretations:

Businesses borrowing to finance capex or additional working cap in expectations of growth

Businesses drawing on credit lines early for fear that the lines won’t be available in a credit event (e.g. GFC 2008)

Corporate bond markets have become less active and therefore some of this has shifted to bank debt.

Overall, all three likely happening anecdotally 2 & 3 seem the larger force.

China

Reopening underway for the last two months. Too early to tell what this means given 1) they all got sick & 2) golden week was also in data (makes for hard comps), 3) these things take time.

The key question is, was is the Chinese economy weak due to zero-covid, or other more endemic factors. If the former, there should be a global growth and inflation impulse, if the latter, then quite the opposite.

Some expecting significant stimulus but that doesn’t seem forthcoming. Similar to the US, the economic prospects seem to hinge on the willingness of Chinese consumers to draw down on excess savings built up during the pandemic. This may not be as straightforward as in the US with the severe contraction in Chinese Real Estate still ongoing(?), and potentially weak export demand creating significant economic uncertainty domestically.

Europe

Mild winter saved Europe from disaster but still required economic self-mutilation.

With Germany posting -0.4% Real GDP in Q4 and -0.9% yoy. As the pillar of economic strength in Europe and a global manufacturing bellwether, this is rather concerning if China reopening does fizzle.

Some data showing euro industrial production held up ok during Q4 which contradicts the above somewhat, need to investigate further, but either way, not ‘strength’.

TTF the benchmark European Natural Gas Hub saw prices rise markedly throughout 2022 as fear of a shortage in winter had governments hitting the offer for whatever price. Obviously, the winter Armageddon didn’t eventuate, however there are remaining ramifications for economic activity going forward:

Gas at EUR47/MWh, this is double the pre-covid average.

Energy utilities need to recoup the cost of the extremely expensive gas they purchased. Depending on the country and policy, some of this will be borne by governments, some will be borne by consumers and businesses.

Overall, the extreme volatility and continued high energy costs will make the operating environment for German/Euro consumers and businesses highly uncertain, which can be a short path to a confidence-induced recession.

Markets

Rates

The “stronger” econ data is increasing short-term inflation expectations and putting upward pressure on yields.

Rates vol has come down a bit recently , which increases ability for levered and insto players to enter rates positions, but many still cautious given uncertain inflation outlook.

Equities

0DTE options, which appear to be a function of regulatory loopholing, seem to be creating localised gravity at the money. This is supressing Vol locally, but could potentially exacerbate a move if the local limits are breached.

Vol and Skew are out of fashion after chronic underperformance in the last few years.

Overall, option markets have become a huge determining factor in the way the equities complex reacts to incoming data.

It appears to my basic understanding that toward the end of a monthly option expiration cycle (and even moreso on monthly and quarterly OpEx dates) option decay flows (Vanna & Charm, for Vol and Time respectively) can dominate overall flows.

Additionally, Gamma effects (depending on overall positioning) can pin markets as OpEx approaches.

Long story short, there appears to be very cyclical windows of weakness and strength in the equities complex which can overpower and influence the reaction to more fundamental type data coming into the market.

US Dollar

Had a strong 2021 & 2022 before retreating significantly at end of year. Potentially turning higher again with US rates, however its hard to know which is leading.

Higher US rates should be $ positive as they attract inflows but many other factors involved.

If trade continues to slow, mercantile $ flows will slow and this should create additional demand in wholesale dollar funding markets.

Simultaneously, if a recession is on the cards, any credit shock will likely significantly disrupt the supple of dollars in wholesale funding markets (via collateral scarcity)

Commodities

Oil is the big one, oil is headline CPI. Oil is off big from its highs which started in March 2022 (yoy comps important for CPIs).

Incredibly difficult to determine the current situation with China not yet reopened. Oil will be a big tell for if the China reopening story is a growth impulse.

Most commodities have been generally rangebound for some time. Not much to say really.